How Many Credit Score Models Are There, In Use?

Did You Know...

There are over 40 versions of the FICO® Score model in existence, with 28 different FICO® Credit Scores commonly used across the three major credit bureaus (Experian, Equifax, and TransUnion).

And because each bureau maintains its own database and applies specific formulas, a single consumer can have over 60 credit scores based on the FICO model alone, depending on the data reported to each agency.

The most widely used versions currently include: FICO® Score 8 and FICO® Score 9 (General purpose) FICO® Score 10 and FICO® Score 10T (Newly released) Industry-specific scores like FICO® Auto Score and FICO® Bankcard Score (ranging from 250 to 900).

Lenders decide which specific version to use based on the type of credit being applied for, meaning a borrower might be evaluated using different scores for a mortgage, an auto loan, or a credit card application...

When Your Credit Scores Are In The Lower Ranges...

As you may already know, borrowing money can become a real challenge. If you are able to qualify for financing in the lower credit score range, bad credit comes at a high cost in terms of the interest rates you’ll pay, increasing all of your payment amounts!

Moving up into a higher credit score range can make a meaningful difference in your financial life. Some benefits of good credit include that it could lift your chances of qualifying for the loans or credit cards you want. It may also make it easier to lease a home or apartment. And, of course, a higher credit score range could save you money in everyway; lower interest rates, lower insurance premiums, lower mortgage payments, lower car payments, lower credit card payments, etc.

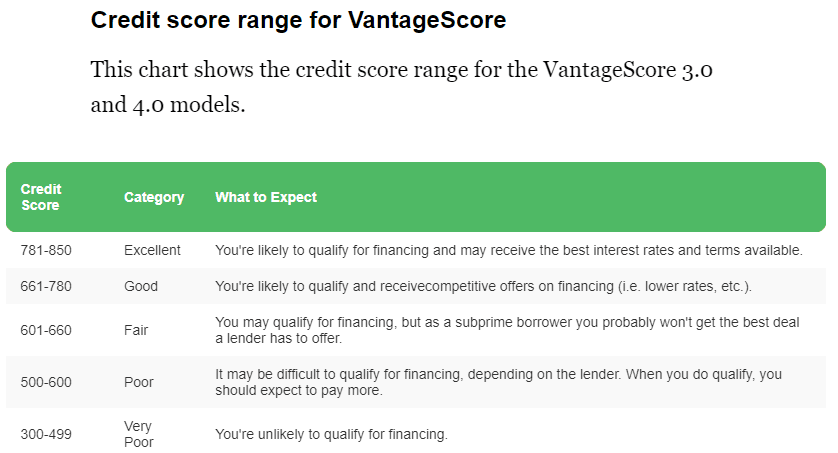

Below is a look at the different Score ranges and a deeper look at the impact your credit score range might have when you apply for financing. Although these ranges are FICO Scores, they can also be a helpful guide when evaluating your VantageScore 3.0 & 4.0 credit scores as well (seen in the image below)...

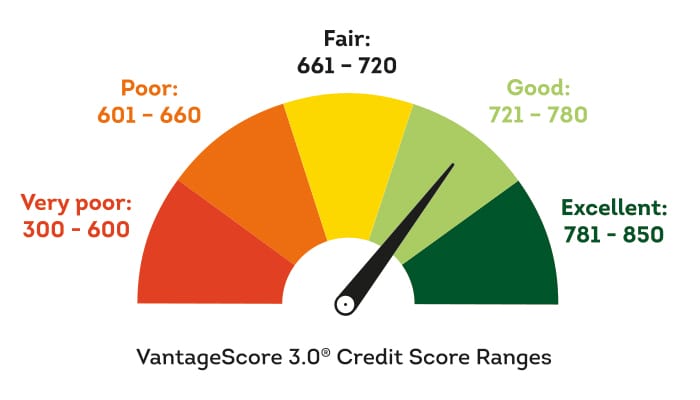

Exceptional Scores (Fico: 800-850)

When you earn a Score between 800 and 850, your credit score is well above average. An exceptional Score tells lenders that you are a responsible borrower with an excellent credit management track record. You most likely have a long credit history, no late payments, low credit card utilization, and you don’t apply for new credit in an excessive way.

At this credit score range, qualifying for new loans (e.g., mortgages, auto loans, personal loans, etc.), credit cards, and other financial products should generally be easy from a credit score perspective. But keep in mind that lenders consider more than just your credit score when you apply to borrow money.

There’s the best chance lenders will offer you their best terms and lowest interest rates when you have an exceptional credit score. Your credit-based insurance scores may also be in great shape which has the potential to help you secure lower auto insurance premiums (depending on your state of residence). These benefits could potentially save you thousands of dollars per year, and much more over the course of your lifetime.

Very Good-Excellent Scores (Fico: 740-799)

Your Score is above average if it falls between 740 and 799. This range indicates to lenders that you’re a responsible borrower and a low credit risk. In other words, you are likely to repay the money you borrow as promised.

With a very good credit score, you should be able to qualify for many types of financing. Lenders may also be willing to extend competitive interest rates and loan terms in an effort to win your business. However, you might not be able to qualify for the lowest rates available depending on a lender’s credit-tiered pricing criteria.

Good-Very Good Scores (Fico: average range 670-739)

If your Score falls between 670 and 739 you have a credit score that is at or near average. As of the third quarter of 2023, the average Score in the United States was 714. [6]Most lenders will consider you to have a good credit score in this range. So, you’re still likely to qualify for many types of financing. However, you could pay more to borrow money since lenders may not offer you their best rates and terms available at this credit score range...

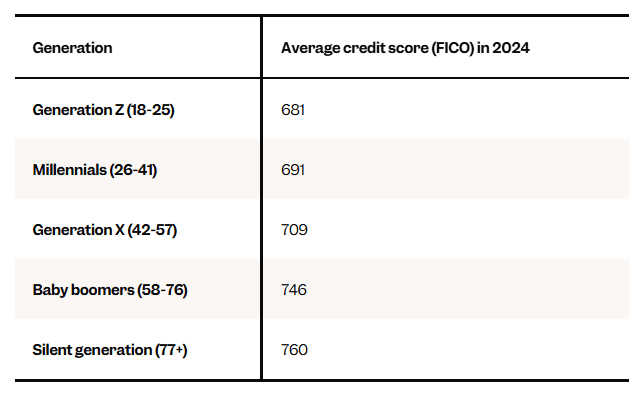

Average Credit Scores By Generation:

Fair or Average Scores (Fico: 580-669)

When your Score is between 580 and 669, you have a score that’s lower than the average U.S. consumer. At this credit score range, lenders may classify you as a subprime borrower. Some lenders may decline your applications for loans, credit cards, and other forms of financing when you have a fair credit score.

If a lender does approve your application, you should expect your interest rate (and potentially fees) to be higher than you could secure with a better credit rating. Over time, higher interest rates could cost you hundreds, thousands, or even tens of thousands of dollars depending on the terms of your loan or credit card.

Poor-Very Poor Scores (Fico: 300-579)

A Score between 300 and 579 is considerably lower than the average U.S. consumer. With a Score in the very poor range, you’re likely to have a hard time qualifying for many types of traditional financing. And when a lender does approve your application for new credit, you may have to accept the least attractive terms, interest rates, and fees available. You may also need to put down deposits when you open new utility accounts or cellular phone services.

If you’re looking to rebuild your credit, you may want to consider some credit building financial products. Credit builder loans and secured credit cards, for example, are two types of accounts that could potentially benefit you over time if you manage them responsibly. Additionally, these products tend to have more lenient approval criteria than traditional credit because of the way they work. As a result, you should find them easier to qualify for when you have very poor credit scores.

No Credit Scores

To qualify for a Score, your credit report must meet certain criteria. Your report must have at least one tradeline (e.g., loan, credit card, etc.) that has been open for up to six months and at least one tradeline that’s been reported to the credit bureau within the last six months. (A single account can satisfy both of these criteria.) There can also be no indication on your credit report that you are deceased.

If you can’t satisfy the criteria above, you will have no credit score. A study by the Consumer Financial Protection Bureau (CFPB) found that some 45 million American consumers have no credit scores either because they don’t have a credit file (26 million consumers) or because the credit files they do have don’t qualify for a credit score.

With no credit scores, it can be difficult to borrow money—especially at affordable rates and terms. Many lenders may be hesitant to approve your applications for financing since you don’t have a previous credit management track record that they can review.

Like consumers with subprime credit scores or very low poor credit scores, you may want to consider establishing some good positive credit history to lift your credit score range. Secured credit cards and credit builder loans are two options that may be a good fit in this credit score range since they offer easier-to-satisfy approval criteria than most traditional forms of credit...

Everyone Can Do This!

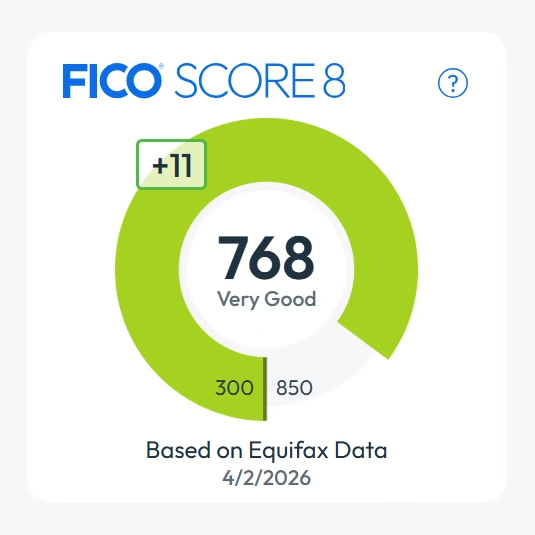

From FICO Score 567 Up to 768

Where-ever your scores are now, they can usually climb much higher a lot sooner than you might think, greatly impacting your financial life in very positive ways!

Get all the factors we suggest you do, where they need to be and watch the life-changing magic happen month after month after month... And still climbing!

We do all the hard work for you, so you can focus on planning your future with much better financial options/choices and less stress, knowing your approval odds are very high for any type of credit...

Plus lowering your monthly living expenses and enjoying more available cash-flow for a better life for you and those you care about.